The homeownership rate gap between White and Black households grew even further in 2020. According to our analysis, the U.S homeownership rate experienced the largest annual increase on record, though Black homeownership remained lower than a decade ago. While homeownership is the principal source of wealth creation, this also may be translated to an even larger wealth gap between White and Black families.

NAR released the 2022 Snapshot of Race and Home Buying report for the third straight year. The main purpose of the report is to address racial inequalities in homeownership at the local level. By identifying these racial inequalities across the country, this could help local communities to find the necessary ways to reduce the homeownership gaps among races. Thus, the report examines how racial disparities in the housing and mortgage market vary by location and how housing affordability differs by race/ethnic group. The report also looks into the characteristics of who purchases homes, why they purchase, what they purchase, and the financial background for buyers based on race.

As 2020 was one of the best years for the housing market, the U.S. homeownership rate climbed to 65.5%, up 1.3% from 2019. Although the homeownership rate for Black Americans also increased to 43.3%, it is still lower than a decade ago. Conversely, White Americans (72.1%), Asian Americans (61.7%) and Hispanic Americans (51.1%) all achieved decade-long highs in homeownership in 2020, with the rate for Hispanic Americans setting a record and reaching above 50% for the first time[1].

[1] The U.S. Census Bureau has recommended to use with caution the 2020 Census products due to the COVID-19 impact on the data collection. The current study used the American Community Survey data. For this dataset, the Census modified their weighting procedures and they adjusted for nonresponse bias by giving more weight to responses from underrepresented groups. Through these changes to their standard weighting process, they have rectified some of the nonresponse bias introduced in the 2020 ACS data due to the pandemic.

Explaining Why Black Homeownership Lags Among any Other Race/Ethnic Group - Higher mortgage denial rates

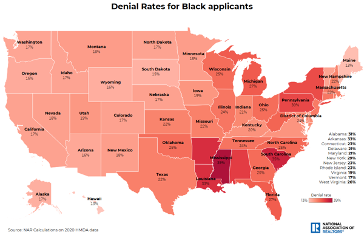

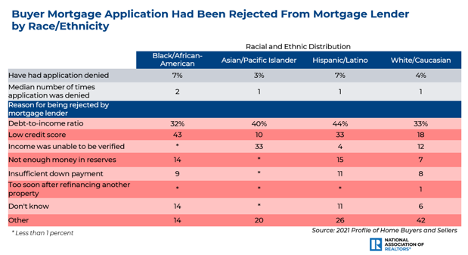

Although mortgage rates dropped below 3% in 2020, not everyone had the same opportunities to get a home loan and benefit from these low rates. Data shows that Black home buyers and owners face extra challenges in getting a mortgage. Denial rates vary significantly by race/ethnic group, with Black Americans having the highest denial rates for purchase and refinance loans. According to our analysis, Black applicants are twice as likely to be denied for a mortgage compared to their White counterparts. While the main reason a mortgage lender rejected their application is the debt-to-income ratio, Black home buyers reported that they also were rejected due to a low credit score. Parsing out by the purpose of loan, denial rates for Black Americans are even higher for home purchase loans. According to the Home Mortgage Disclosure Act (HMDA), nearly 27% of the loan applications for a home purchase were denied compared to 20% which is the denial rate for refinancing.

At the local level, the denial rate is disproportionately high for Black homeowners and buyers in those states with high concentrations of Black households. Low income seems to be the main reason that more Black households were denied mortgages in these areas. Specifically, in the top 10 states with the highest denial rates, the median income of Black applicants was $62,990 on average. For instance, the median income for Black households was $51,760 in Mississippi, which was the state with the highest denial rates in the country. However, as income increases, denial rates drop. In the top 10 states with the lowest denial rates for Black households, the median income of those applicants was $81,440. For example, the median income of Black households that applied for a mortgage was $102,830 in Hawaii, the state with the lowest denial rates for Black households.

-Lower affordability

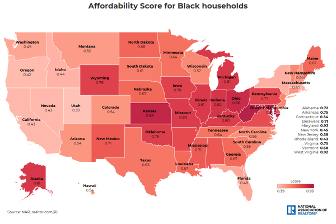

In the meantime, during the pandemic, rising home prices and low housing supply have disproportionally impacted Black households more than any other race/ethnic group. According to our “Double Trouble” report, White households are 40% more likely to be able to afford to buy a home compared to Black households. Nationwide, households with incomes of $100,000 or more can afford to buy at least roughly half the homes that were listed for sale. But, while 35% of White households have that income, only 20% of Black households do. So, due to lower income, affordability for Black households is the lowest compared to any other race/ethnic group. For instance, the affordability score in the District of Columbia is 1.4 for White households but only 0.5 for their Black counterparts. Respectively, the affordability score for White households is 1 in Wisconsin compared to 0.6 for Black households.

-Lower affordability for renters

Data also shows that Black renter households are more squeezed than any other race/ethnic group. One in two Black renter households spend more than 30% of their income on rent. And about 28% of Black renter households spend more than 50% of their income on rent, representing nearly 2.3 million households. In contrast, 21% of White renter households are severely cost burdened, spending over 50% of their income on rent. This translates to about 4.9 million White renter households. Although they have a lower income (30% lower) than White renters, their monthly rent isn’t significantly lower than that of White renters. In 2020, the median income of Black renter households was $31,700, compared to $45,200 for White renter households. In the meantime, the average monthly rent was $1,010 for White compared to $830 for Black renter households. While rental cost is expected to rise even further in 2022, it will be more difficult for Black renter households to save for down payment for a home purchase.

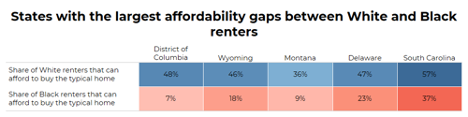

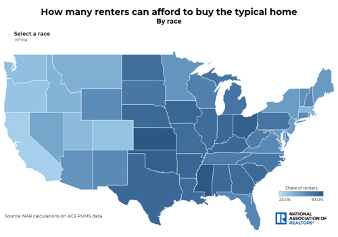

After comparing the qualifying income needed to purchase the typical home by state to the median income of renter households, the National Association of REALTORS® was able to estimate how many of these renters can afford to buy the typical home. It’s interesting to see that while nearly 50% of the White renter households can afford to buy the typical home, only 36% of the Black renter households can do the same, nationwide. At the local level, the gap between White and Black renters’ affordability is even larger in the following areas:

Select a race to see how many renter households can afford to buy the typical home by state:

Home Buyer Demographics by Race/Ethnicity

Looking into data from the 2021 Profile of Home Buyers and Sellers report, we can further see the characteristics of recent home buyers by race and ethnicity, and see ways the home buying process differs compared to the previous year. Among all home buyers, White/Caucasian home buyers made up the largest share at 82%, followed by Hispanic/Latino (7%), Asian/Pacific Islander (6%) and Black/African-American home buyers (6%), and Other at 2%. We see the largest share of married couples at 70% among Asian/Pacific Islander home buyers, and the largest share of single female home buyers were among Black/African-American home buyers (33%). We also see the highest share of first-time buyers among Asian/Pacific Islanders at 56%, and 49% of Black/African American buyers.

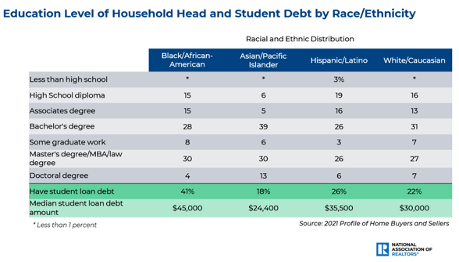

Black/African African-American home buyers reported the highest share of student loan debt at 41%, with a typical student loan debt amount of $45,000. Hispanic/Latino home buyers reported a median student loan debt amount at $35,500, with 26% reporting they had student loan debt. This is compared to just 22% of White/Caucasian and 18% of Asian/Pacific Islander buyers reporting that they have student loan debt.

We continue to see help and assistance from family and friends among recent buyers, with 22% of White/Caucasian, 21% of Hispanic/Latino, and 20% of Asian/Pacific Islander first-time home buyers lived with parents, relatives, or friends prior to purchasing their home. This is compared to only 15% of Black/African-American first-time home buyers who lived with parents, relatives, or friends prior to purchasing their home. Additionally, we saw that 25% of Asian/Pacific Islander buyers used a gift or loan from a relative or friend towards their down payment, which is up from 20% last year. When making their down payment, 58% of Black/African-American home buyers used their savings, up from 50% last year.

Home Buyers and Fair Housing

Additionally, recent buyers were asked if they had experienced or witnessed discrimination during their real estate transaction. Looking at ways recent home buyers witnessed or experienced discrimination in a real estate transaction, the most common was being steered towards or away from specific neighborhoods, which was reported at higher rates compared to the previous year. We saw 50% of Hispanic/Latino, 48% of Asian/Pacific Islander, and 46% of Black/African/American buyers reported steering towards or away from specific neighborhoods. This is compared to the 2021 report where 34% of Hispanic/Latino, 28% of Asian/Pacific Islander, and 30% of Black/African/American buyers reported steering towards or away from specific neighborhoods. This year we added the option for “appraisal of home” as a possible discrimination that could be witnessed or experienced. Nine percent of Asian/Pacific Islander, 6% of Hispanic/Latino and White/Caucasian, and 5% of Black/African/American buyers reported witnessing or experiencing discrimination through a home appraisal.

When asked if they had experienced discrimination in a real estate transaction, 7% of Black/African-American, 6% of Hispanic/Latino, and 4% of Asian/Pacific Islander home buyers experienced discrimination based on race. Three percent of Black/African-American, and 2% of Asian/Pacific Islander and Hispanic/Latino home buyers experienced discrimination based on color. While 39% percent of Black/African-American, 38% of Asian/Pacific Islander, 36% of Hispanic/Latino, and 28% of White/Caucasian home buyers did not experience discrimination in their real estate transaction they still believe that it exists.

If you're looking for more research and statistics, go to Industry Research & Trends in the REALTOR® Store.